In a previous article, I provided an introduction to business forecasting. In this article, we will discuss 2 types of forecasting models – the weighted and unweighted moving average model. I’ll also discuss Measure of Forecasting Accuracy. In another article, I showed how to conduct a regression analysis in a call center.

Unweighted Moving Average

The Moving Average model is in class of “naive” models, because it takes a data set with variation and creates another data set with less variation, or a smoothed data set. The Moving Average model takes the average of several periods of data; the result is a dampened or smoothed data set; use this model when demand is stable and there is no evidence of a trend or seasonal pattern.

Moving average routines may be designed to remove the seasonal and random noise variation within a time series. If the moving average routine is used repeatedly on each newly-generated series, it may succeed in removing most of any cyclical variation present. What is left of the original series after early smoothings to remove seasonal and random or irregular components is a successor series retaining some combination of trend and cyclical behavior. If no trend or cyclical behavior are present in the time series, the smoothings may leave a successor series which plots as a nearly horizontal line against time on the horizontal axis. Assuming the presence of trend and cyclical behavior in the original series, the moving average process provides a method of isolating it.

The smoothing effect of the moving average model provides for a “cleaner” data set, which may or may not help in estimating the future level of a variable.

The formula for the Moving Average Model is below:

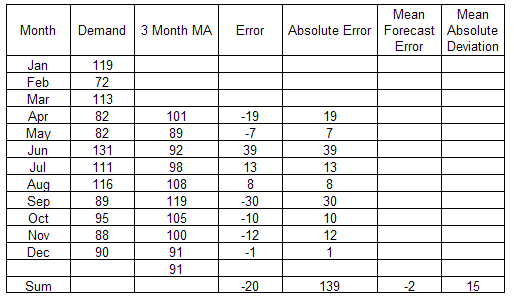

Let’s suppose the data set below:

The Month and Demand columns shows the time series for the month. The 3rd column shows the 3 period moving average, calculated as follows:

((119 + 72 + 113) / 3 = 101)

Following the same formula above, walk across the time series in 3 week periods in order to build the smoothed series, the new time series with less variation.

Forecasting Measures of Accuracy

The 4th column shows an Error column calculated as follows:

((Demand – 3 Week MA) = Error)

The 5th column shows the Absolute Error, which is just the absolute number of the items in the Error column.

The 6th column shows a Mean Forecast Error, or MFA. This shows the direction of the forecasting error. The rule here is that if the number is negative, the the model tends to over-forecast. If the number is positive, then the model tends to under-forecast. The MFA is calculated as follows:

Sum of Error / N = MFA

Using the data set above,

[((-19 + -7 + 39 + 13 + 8 + -30 + -10 + -12 + -1) / 9) = -2]

Since the MFA is negative, then this tells us that the direction of the forecast error; in this case, the data and using this model tends to over-forecast.

The last column shows a Mean Absolute Deviation, which gives us an indication of the size of the error. In other words, since MFE for our data set is negative, pointing to an over-forecast, the MAD tells us that the average size of that over-forecast is ~15. To calculate MAD, do the following:

Absolute Error / N = MAD

In other words,

[((19 + 7 + 39 + 13 + 8 + 30 + 10 + 12 + 1) / 9) = 15]

The smoothed time series above coupled with MFA and MAD gives us more context around our point estimates and forecast accuracy. This enables the firm to better plan for the future and form strategies around labor, capacity, inventory, service levels, and other pertinent items important to the firm.

Weighted Moving Average

Follow the steps for the Moving Average model above. Weights on this model indicates the subjective importance we wish to place on past or recent data. Weights can be from 0.0 to 1.0; the higher the weight, then the higher importance we are placing on more recent data; similarly, for lower weights.

In forming your moving average time series, just add a weight multipier to form the new, smoothed-out time series. All remaining steps in the Moving Average Model are the same.

Become a Lean Six Sigma professional today!

Start your learning journey with Lean Six Sigma White Belt at NO COST

: Are You Monitoring the Behavior?")

Beth says

Hi,

LOVE your Post. Was wondering if you could elaborate futher. We use SAP. In it there is a selection you can choose before you run your forecast called initialization. If you check this option you get a forecast result, if you run forecast again, in the same period, and do not check initialization the result changes. I can not figure out what that initialization is doing. I mean, mathmatically. Which forecast result is best to save and use for example. The changes between the two are not in the forecasted quantity but in the MAD and Error, safety stock and ROP quantities. Not sure if you use SAP.

Thanks so much.

Beth

jaspreet says

hi

thanks for explaining so effeciently its too gd.

thanks again

Jaspreet